What Does Blockchain Mean for Small Businesses?

If you have ever felt overwhelmed by the speed with which the world is changing, you are certainly not alone. The amount of news and information we are battered with on a daily basis, often gives us that anxious feeling of whether we can keep up or not.

Being unable to spend your days browsing the net for the most recent developments, it is important to pick those headlines that are the most relevant for you.

For that reason, blockchain is on today’s agenda. Controversial, mysterious, and complicated; these are only some of the words used to describe blockchain.

Mysterious: No one can really tell who is behind the development of blockchain. The first person (or persons) to conceptualise the technology do so under the alias Satoshi Nakamato. Whether it is an individual or a group behind the alias is still unknown. However, Nakamato designed Bitcoin (cryptocurrency), of which blockchain is an underlying technology.

Controversial: Blockchain is undermining all of the existing standards in place for conducting and recording transactions thus far. It is particularly challenging for banks who already have trouble keeping up with the changing ecosystem. Institutionally, they are not capable of innovating quickly, making it more difficult for them to introduce new solutions and keep up with their new competitors.

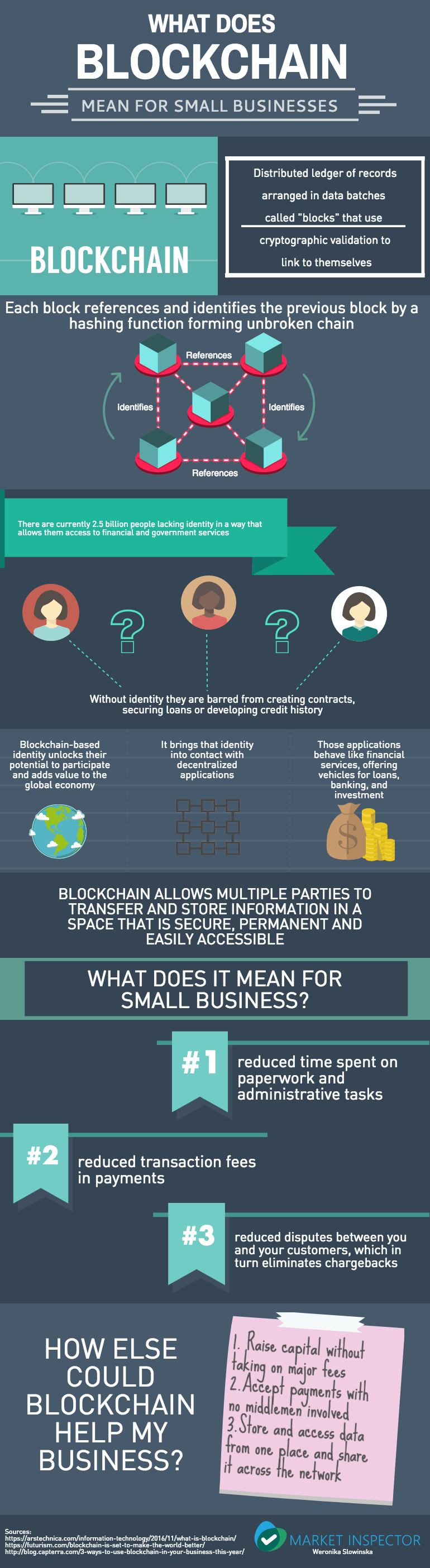

Complicated: Starting to learn about blockchain is like trying to solve sudoku for the first time. At the beginning, it might appear complicated but, eventually, it makes sense. Blockchain is a decentralised ledger in which data batches (blocks) use cryptographic validation to link themselves together. It is based on a mathematical equation which actually acts as an authority. It exists on multiple computers at the same time in such a way that anybody with an interest can maintain a copy of it, and can only be changed when there is a consensus among the group. Moreover, old transactions in the ledger are preserved forever and new transactions are added to it irreversibly.

Blockchain, as a ledger system, automates and records transactions which can be accessed by all the parties involved in the payment or lending processes. Getting business loans or making, and accepting, payments would cost little, or nothing. Moreover, Blockchain eliminates the need for saving copies of invoices, bills and financial statements, as it is all on the ledger. This system has the potential to make the lives of individuals, as well as business owners, much easier.

We strive to connect our customers with the right product and supplier. Would you like to be part of Market Inspector?