Is Peer-to-Peer Lending a Safe Option for Your Business?

As an entrepreneur or owner of a small business, finding adequate funding can be quite a challenging task - which is precisely why business loans are so useful!

Coming in many shapes and variations, business loans can provide crucial help with starting, managing, or further developing a business. As one of the most widely acknowledged and broadly used ways of funding businesses, business loans typically involve an agreement between a lending institution and a borrower.

What Is Peer-to-Peer Lending?

One of the most popular upcoming ways of lending money for businesses is the so-called method of peer-to-peer lending. But how, exactly, can peer-to-peer lending be defined?

In general, it refers to a way of borrowing money that effectively cuts out banks as a middleman between the borrower and lending institution.

Peer-to-peer lending sites basically work as platforms with the purpose of bringing the two (or more) parties together, connecting people who want to invest money with a diversified risk to those who need the money to fund their business or project.

In the UK, the concept of peer-to-peer lending emerged roughly ten years ago, and while it was initially met with some skepticism, British peer-to-peer lending sites such as Zopa or Funding Circle are counted among the largest and most successful platforms today. Just to have a comparison, the three main British peer-to-peer lending sites had released more than £250 million in loans by June 2012.

While this method of lending money often attracts both lenders and borrowers by promising top returns of 7-12pc, criticism has, of course, also been voiced. So while peer-to-peer lending might be a good and innovative option for some, others might prefer to stay away and pursue more classical, secured ways of funding - according to experts, it all depends on how much risk you are willing to take.

Since any sort of decision about getting a business loan needs to be well researched and thought out, let us make part of it a little easier by taking a closer look at the option of peer-to-peer lending.

Alternative Ways of Business Funding - New Trends and Innovations

When applying for a traditional business loan, owners of small businesses or startups often face inconveniently lengthy application processes, which can act as an off putting factor - especially when the need for funding is rather more urgent. Also, getting traditional secured loans quickly and easily often involves having to deal with higher repayment rates in return.

These are just a few of the reasons why many young entrepreneurs and small business owners are increasingly turning towards alternative ways of funding, often also referred to as social or crowdfunding loans.

Who Should Consider Alternative Funding?

As already mentioned, alternative ways of business funding, such as online loans, crowdfunding, or peer-to-peer lending, offer some attractive features for lenders and borrowers alike - however, they are not everyone’s cup of tea, so make sure to conduct some thorough research and revise all of your options before making a decision.

Experts in the field such as Martin Lewis, founder of MoneySavingsExpert, say that while there is a possibility of receiving top returns, people should be aware of the fact that this is by no means guaranteed. In his article for the Telegraph, he cautions that it should not be confused with saving, placing it “[...] somewhere in between saving and investing”.

With these cautions in mind, alternative ways of funding can be a great option for small- or medium-sized businesses who need funds rather more promptly, and smaller projects by artists, designers, and developers (such as apps, for example).

Especially for projects which are a little more outlandish or ambitious, alternative funding platforms can additionally provide a good option for doing some initial market research - would people actually be interested in - and be willing to pay for this new product I have in mind?

Finally, many lenders and investors have simply become more skeptical towards banks, a trend which has grown particularly after the 2008 collapse of Lehman Brothers. Proof that even large banks can crash, destabilising entire economies in the process, has shaken many people’s trust and inspired more and more lenders and borrowers to turn towards alternative ways of funding.

What about Bad Credit?

It is also precisely because of the aforementioned crisis of 2008 that banks have generally become more cautious about awarding business loans to borrowers with bad business credit. Due to UK regulations, it is mostly rather hard for small business owners to determine whether their credit score is adequate for being granted a secured business loan. While receiving a traditional business loan with bad credit is still possible, it usually entails higher interest rates and a larger amount of collateral. Thus, it might be worth turning towards alternative ways of lending, which have somewhat dissolved the relevance of the bad credit issue over the past few years.

While peer-to-peer lending platforms perform a careful screening of potential borrowers, small business owners who have somehow accumulated bad credit might nevertheless be able to find a better arrangement for getting their business back on track via alternative funding methods.

Lenders are generally made aware of the higher risk involved in funding such borrowers, sometimes via a system of categorisation, but they might still decide to back a project they find promising.

The Pros and Cons of Peer-to-Peer Lending

As the previous sections already indicate, peer-to-peer lending represents a new, innovative way of funding which has nevertheless also sparked its fair share of controversy. Some people perceive it as a great chance to be less dependent on large banks, to boost business in a tricky situation, or to diversify their financial risk. Others, however, see the promise of top returns as a cheap lure, accusing platforms of not performing proper credit checks on borrowers.

The shutdown of the platform Quakle has especially shaken people’s trust considerably, since it left some lenders with having to chase down their money from borrowers individually.

Between all these arguments, it may seem impossible to make a good, well-informed decision. But no worries - we have gone through the pros and cons of peer-to-peer lending and specifically listed them for you, together with an overview of the most popular lending sites.

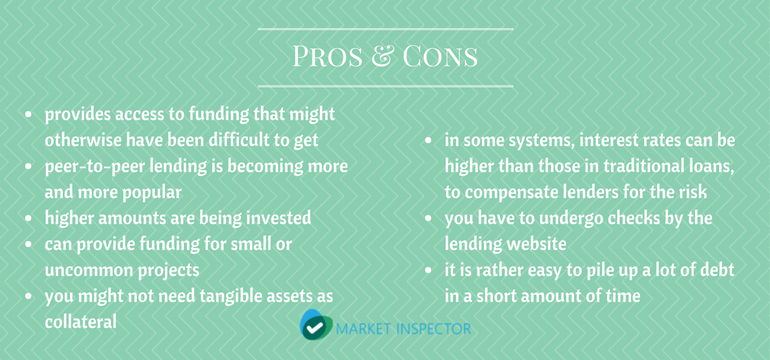

For Borrowers

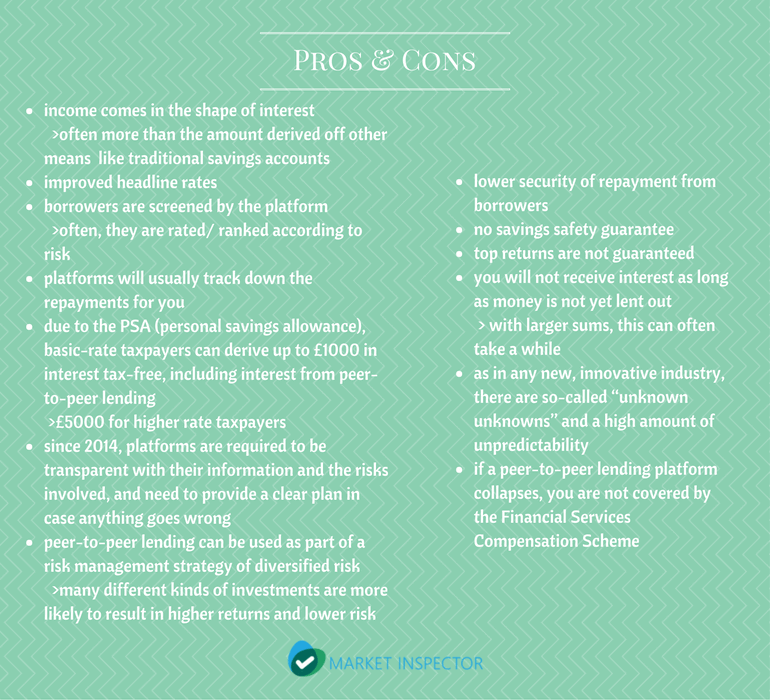

For Lenders

In the end, it bears repeating that especially lenders should be aware that peer-to-peer lending is not the same as saving.

When choosing your preferred platform, it is also well worth considering that lending sites employ different techniques in order to mitigate risk. Here is a short list of the largest and most popular peer-to-peer lending sites in the UK!

Peer-to-Peer Lending Sites

Safety Concerns

As the overview above suggests, peer-to-peer lending as an innovative way to lend and borrow money provides its clients with many chances - but safety concerns are high as well, particularly among traditional bankers. They caution that platforms may allow loans to flow towards the same borrower over a rather short period of time, so that individuals can easily pile up a lot of debt.

There are also issues with transparency, with critics striving to ensure, somehow, that platforms lend out the money they receive responsibly. Additionally, some unsecured loans given out via peer-to-peer lending are gigantic, which has fuelled further criticism.

The biggest fear, however, seems to be that uninformed lenders keep pushing ever more money into lending sites without knowing all the risks.

Find the Best Option for Your Business

In the end, the most important safeguard when dealing with peer-to-peer lending is good research and a general awareness of the risks involved.

All things considered, it is ultimately up to you to decide whether peer-to-peer lending is a safe option for your business and its individual situation. So make sure you are aware of the different ways to receive funding for small business in the UK and assess your specific situation thoroughly.

We strive to connect our customers with the right product and supplier. Would you like to be part of Market Inspector?